A buy-sell agreement is a legally binding contract in which the owners of a business set forth the terms and conditions of a future sale or buy back of a departing owner’s share of the business. Specifically, buy-sells control when owners can sell their interests, who can buy an owner’s interest, and at what price.

Buy-sells can accomplish many objectives, but are primarily used to ensure the smooth continuation of a business after a potentially disruptive event, such as an owner’s retirement, incapacity, or death.

Also valuable estate planning tools, buy-sells can provide for the orderly succession of a family business, and for the liquidity needed for payment of a deceased owner’s estate settlement costs and taxes. Further, if structured properly, a buy-sell can establish the purchase price as the taxable value of an owner’s business interest, avoiding unexpected estate tax consequences at the owner’s death.

WHAT IS A BUY-SELL AGREEMENT?

Buy-sell agreements are very important planning tools that can accomplish many things for a business with two or more owners. Sometimes referred to as a prenuptial or premarital agreement among business owners, a business continuation agreement, a stock purchase agreement, or a buyout agreement, a buy-sell is a legally binding contract that establishes when, to whom, and at what price an owner, partner, or shareholder can sell his or her interest in a business.

A typical buy-sell allows a business entity or other business owners the opportunity to purchase a departing owner’s business interest at a predetermined price. This allows the business and the remaining owners to protect themselves from future adverse consequences, such as disruption of operations, entity dissolution, or business liquidation that might result if certain events, such as an owner’s sudden incapacity or death should occur. This can also minimize the possibility that the business will fall into the hands of outsiders.

The ability to fix the purchase price as the taxable value of a business interest makes this tool especially useful in estate planning. Agreeing to a purchase price while all parties are alive minimizes the possibility of unfair treatment to a deceased owner’s heirs. And, the IRS’ acceptance of this price as the taxable value can help minimize estate taxes on the deceased owner’s business interest.

Additionally, because funding for buy-sells is typically arranged when the buy-sell is executed, the possibility that funds will not be available when needed is minimized, and a deceased owner’s estate can be provided with needed liquidity for expenses and taxes.

Tip: Buy-sells are also used to give a business and co-owners the right to buy out an owner (force an unwilling owner to sell), or to give an owner the right to force the business or co-owners to buy him or her out.

HOW DOES A BUY-SELL AGREEMENT WORK?

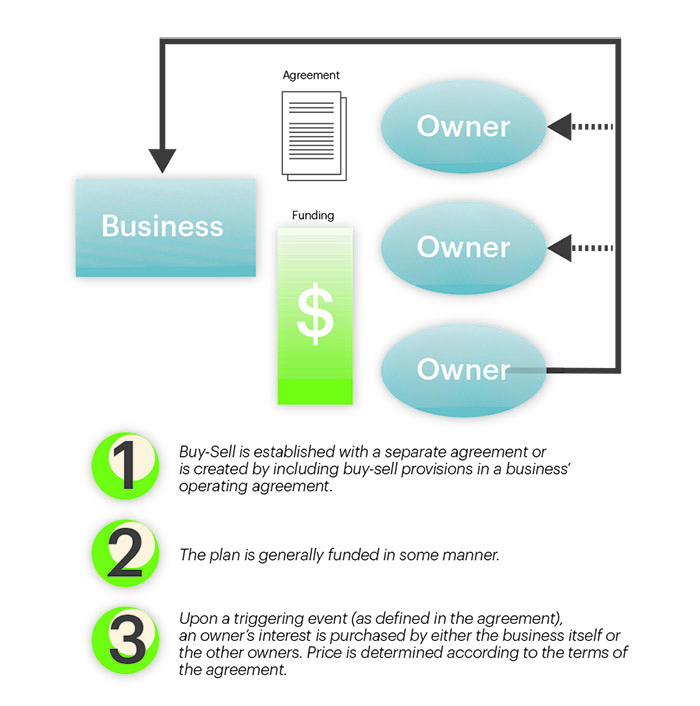

A buy-sell can be a separate agreement or can be created by including buy-sell provisions in a business’ operating agreement.

A buy-sell must clearly identify the potential buyers, any restrictions and limitations, and the conditions under which a sale will occur. Sale triggering events typically include:

A buy-sell should set forth the purchase price or a formula for determining the purchase price. Without establishing this price in advance, lengthy disputes and lawsuits can arise at the time the ownership interest must be bought back.

Fixing the estate tax value of a business interest

One of the advantages of buy-sells is the ability to fix the purchase price as the estate tax value of a deceased owner’s business interest, which can help avoid future valuation problems with the IRS. When using a buy-sell to set the estate tax value of a business interest, careful drafting is essential. To pass muster, all buy-sells must pass the following four-part test:

When the buy-sell involves family members, it must also be proven that the transaction is comparable to arms-length sales between unrelated persons, and was entered into for a bona fide business purpose.

Caution: Determining the fair market value of a business may require an independent business valuator. The IRS can impose harsh penalties for understating the value of an asset for estate tax purposes.

Financing the buyout

For a buy-sell to be successful, funds must be available to carry out the terms of the buy-sell. Without a funding plan in place, the buyer(s) may be forced to sell assets, take out loans, or even file for bankruptcy.

There are several ways to fund a buy-sell, including:

Factors that generally influence the choice of funding method include:

Depending upon the specific details, there might be just one funding method that is appropriate, or there may be several funding methods that could be used.

Structuring buy-sells

Buy-sells can be structured to meet the needs of both the business and the owners, taking into consideration tax consequences and individual goals. There are four basic structures for buy-sells, and some combinations are possible. Very brief descriptions of the four basic structures follow.

Tip: It is not necessary that the same buy-sell apply to all the owners of a business.

SUITABLE CLIENTS

EXAMPLE

Steve and Jack are brothers who loved cars as teenagers. Steve could fix just about anything and Jack went to all the car shows and talked to anyone who would listen about the new models.

As soon as they graduated college, Steve and Jack borrowed some money and bought a car dealership. Over the years, they built a very successful business–Steve ran the operations while Jack took charge of sales and marketing.

While their business thrived, their personal lives flourished as well–each marrying and having several children. But then, one day, Jack unexpectedly had a heart attack and died. Jack’s family was overwhelmed with shock and grief. After several weeks, Jack’s widow, Norma, came by Steve’s office. Norma was very nervous–she needed to broach the subject of her husband’s interest in the dealership, but knew Steve was having a difficult time managing the business on his own. Norma was having her own financial difficulties, however, having a large mortgage to pay and two children in college. She couldn’t put off this meeting, even if it resulted in tension and bad feelings.

To her delightful surprise, Norma soon discovered how much foresight her husband and brother-in-law possessed. They had executed a buy-sell agreement many years ago, just in case such an unfortunate event should occur, and financed the agreement with life insurance policies on each other’s lives. Steve was in the process of claiming the proceeds and would pay Norma the agreed-upon purchase price.

Norma received her rightful share of the business, in cash, with which she was able to meet her family’s needs. Steve was able to continue the business with no interference. And though it wasn’t quite the same, he hired a sales and marketing manager to take over his brother’s duties, and the dealership continued to operate successfully.

ADVANTAGES

DISADVANTAGES

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable.

HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources. HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.